Why is India’s Credit Card Penetration Still Under 5%?

India is a global leader in digital payments, yet credit card penetration remains stuck in a structural bottleneck. While we recently crossed the 100 million card milestone, the unique user base remains small. This isn’t a lack of demand; it’s a fundamental cultural and structural shift in how India chooses to borrow.

In this edition, we analyse:

- The Infrastructure Gap: Why 731 million QR codes have outpaced 12 million POS terminals.

- Cultural Debt-Aversion: The shift from "revolving credit" to "pay-now" ecosystems.

- The Informal Bottleneck: How rigid documentation excludes the self-employed class.

- The 2026 Pivot: Why "Credit on UPI" is the real growth engine for the next decade.

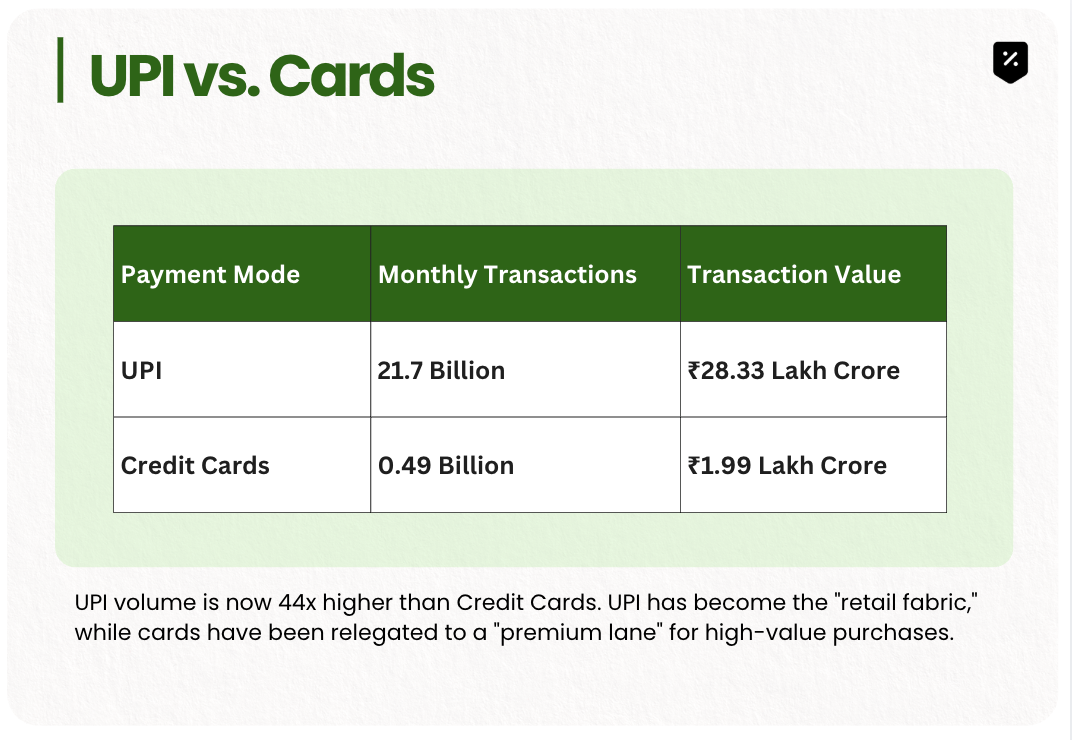

UPI volume is now 44x higher than Credit Cards. UPI has become the daily utility, while cards remain a premium lane. This divergence stems from the Indian consumer's inherent debt-aversion, the cultural preference to spend from an existing bank balance rather than revolving a high-interest credit line.

Segment 1: Infrastructure Barrier: 60 to 1

Credit cards require expensive Point-of-Sale (POS) hardware. In contrast, the zero-cost interoperability of QR codes has allowed digital payments to penetrate deep into rural markets where a physical card machine is non-existent.

Physical vs. Digital Footprint

- Active UPI QR Codes: 731 Million

- Physical POS Terminals: 12 Million

For every 1 card machine, there are 60+ QR codes active.

The POS terminal is a Tier-1 city phenomenon. For a merchant in a Tier-4 town, the maintenance, MDR fees, and connectivity issues of a POS machine make it unviable. The QR code has effectively leapfrogged the card era for 90% of Indian small businesses.

Segment 2: Eligibility Trap

Traditional credit cards rely on rigid documentation, ITRs and salary slips. This creates a glass ceiling for the rising self-employed class and the informal workforce.

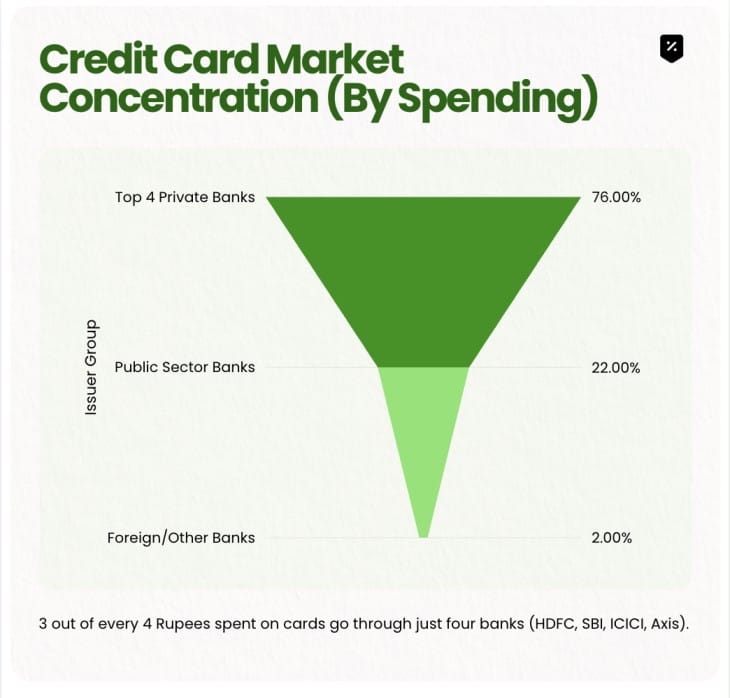

This concentration proves that credit is currently an "elite club." While the top 50 million urban professionals are over-leveraged with multiple cards, the "Next 500 Million"freelancers, small shop owners, and gig workers, remain excluded because they lack formal pay slips, even if they have the cash flow to repay.

The industry has realized that the physical card is the bottleneck. The solution? Credit on UPI. By linking RuPay Credit Cards directly to UPI apps, the industry is finally bringing credit to the QR codes that already exist everywhere.

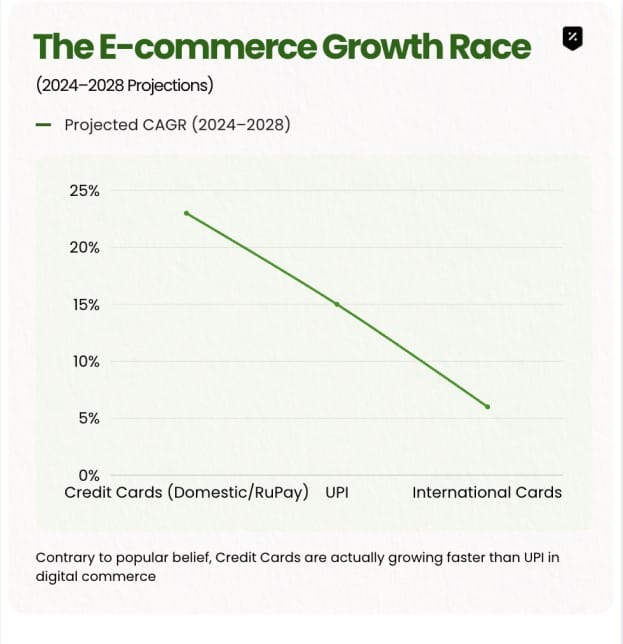

We are seeing a "Two-Speed Economy." People use UPI for daily essentials (tea, groceries), but they are increasingly using Credit-linked UPI for e-commerce and electronics to capture rewards and EMI benefits. Credit is growing by "piggybacking" on the habits UPI already built.

Conclusion: The Evolution of Borrowing

The "under 5% penetration" headline is a legacy metric. In reality, credit in India is moving away from the plastic in your pocket and into the code of your payment apps.