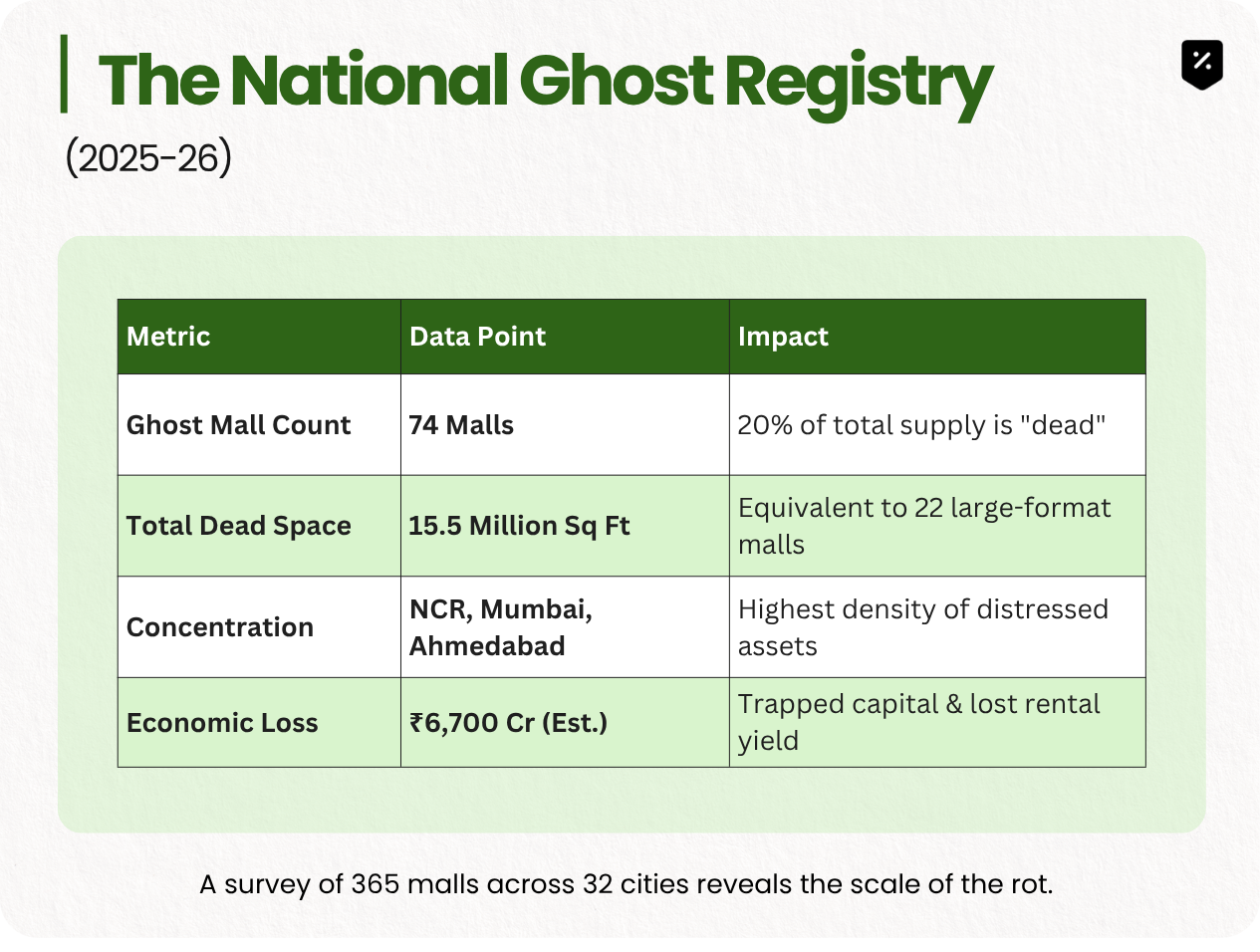

Why is 15.5 million sq ft of Indian retail sitting dead in "Ghost Malls"?

While headlines focus on the "Premiumisation" of Indian retail and the waitlists for space in DLF or Phoenix malls, a silent crisis is rotting in the suburbs. Nearly one-fifth of India’s operational shopping centres have officially become Ghost Malls.

These are the carcasses of India’s first speculative retail bubble 74 structures across 32 cities that stand as monuments to bad design, fragmented ownership, and poor capital allocation. In a country where brands are desperate for space, 15.5 million square feet of retail real estate is effectively a graveyard.

In this edition, we analyse:

- The Ghost Count: Breaking down the 15.5 million sq ft vacancy.

- The "Strata-Title" Trap: Why fragmented ownership makes revival impossible.

- Tier-2 Paradox: High brand demand vs. zero "Quality" supply.

- Capital Misstep: What the bust tells us about the future of commercial RE.

Segment 1: The Anatomy of a Ghost Mall

A Ghost Mall is defined by a vacancy rate of 40% or higher. These aren't just empty buildings; they are failed ecosystems. Most were built during the 2005–2012 boom, characterised by a build it and they will come philosophy that ignored catchment demographics and tenant mixing.

Segment 2: Why Can't We Fix Them?

The biggest hurdle to reviving these assets isn't architecture, it's Strata-Titled Ownership.

In the first wave of construction, developers sold individual shop units to hundreds of small investors to fund construction.

- The Gridlock: To renovate or reposition a mall, you need consensus. When 300 different people own 300 different shops, agreeing on a new anchor tenant or a layout change becomes a legal nightmare.

- The Comparison: Successful malls (Grade-A) are usually Lease-only models owned by a single institutional developer (like a REIT or a Global PE firm) who controls the brand mix.

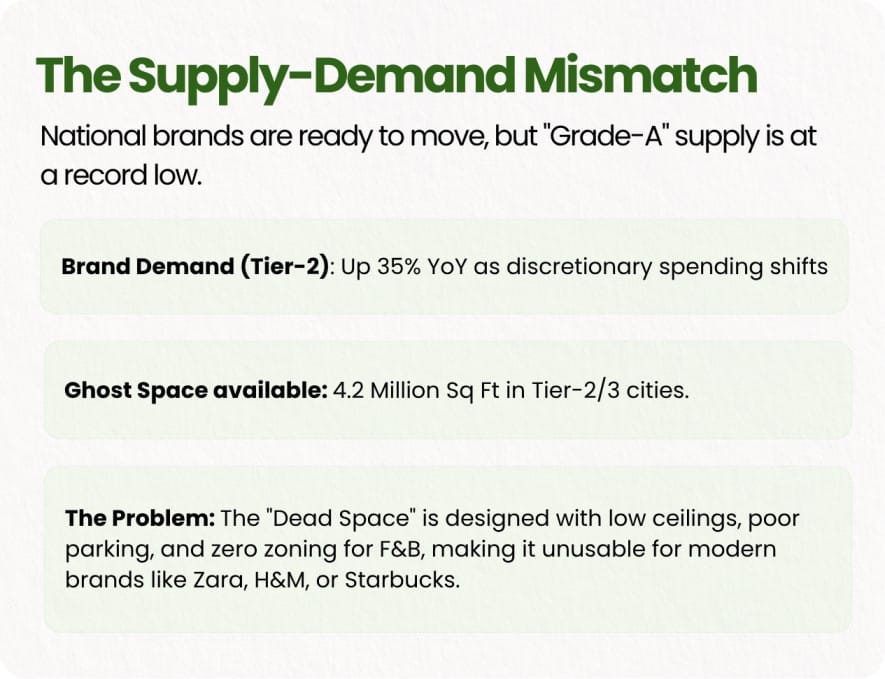

Segment 3: The Tier-2 Paradox

There is an incredible irony in the data: National and international brands are currently starved for space in Tier-2 cities, yet these same cities are littered with ghost malls.

Segment 4: The Afterlife of Dead Malls

What happens to 15.5 million sq ft of concrete carcasses? We are seeing the first signs of Adaptive Reuse.

- Warehousing: Converting dead basement/ground levels into Dark Stores for quick-commerce.

- GCC Conversion: Converting upper floors into low-cost Global Capability Centers or Co-working hubs.

- Demolition for Residential: In prime NCR and Mumbai pockets, the land is now worth more than the structure.

The Hard Lesson for Capital

The story of India’s ghost malls is a warning against speculative retail-strata investing. Real estate isn't just about four walls; it’s about managed ecosystems. At Per Annum, we believe the Ghost Mall era is finally ending as capital becomes more institutionalized. Today, the focus has shifted to SM REITs and single-owner Grade-A assets where the "dead space" risk is mitigated by professional management and long-term lease structures.

The carcasses remain, but the smart money has moved on.