Why a Rate Hike in Tokyo Just Triggered a Sell-off in Mumbai?

For the average investor in Dalal Street, Tokyo feels worlds away. We focus on the RBI, the Fed, and the Nifty 50. But in a hyper-connected 2026, the Indian stock market is tethered to the Bank of Japan (BoJ) by a very thin, very expensive wire called the carry trade.

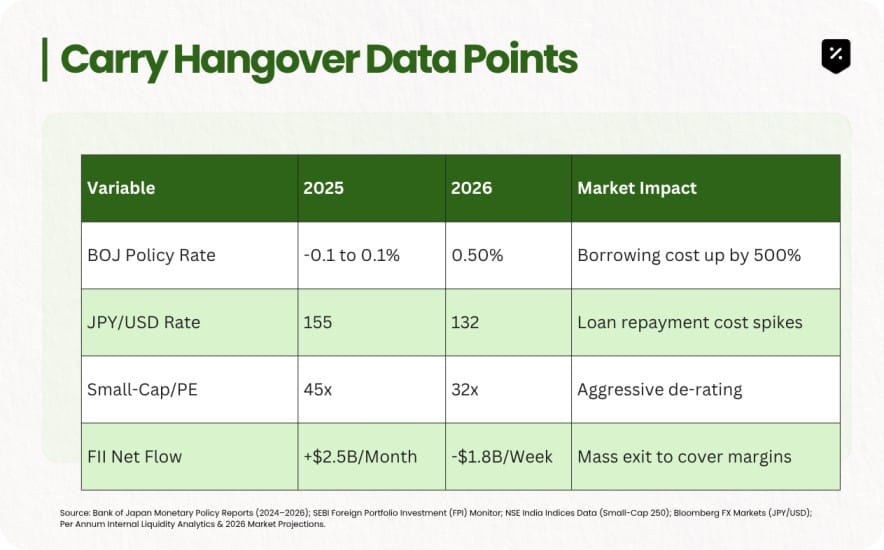

This week, that wire snapped. When Tokyo hiked rates to a staggering 0.50%, it didn't just affect Japanese homeowners, it pulled the rug out from under the speculative froth in Mumbai’s small and mid-cap segments.

In this edition, we will analyse:

- The Arbitrage Engine: How free money in Yen fueled the Indian bull run.

- The Margin Call: Why a stronger Yen forces global funds to sell their Indian winners.

- The Small-Cap Victim: Why the most speculative corners of the NSE are the first to bleed.

- The Liquidity Outlook: Is the cheap money era officially dead?

Segment 1: What is the Yen-Carry Trade?

The mechanics are deceptively simple. For decades, Japan had near-zero or negative interest rates.

Borrow: Global hedge funds borrow billions in Japanese Yen at 0.1% interest.

Convert: They sell those Yen and buy high-yielding currencies like the US Dollar or Indian Rupee.

Invest: That money flows into hot markets; primarily Indian Equities and US Tech.

As long as the Yen stays weak and Japanese rates stay low, the carry is free profit. But when the BoJ hikes rates, the cost of that borrowed money goes up, and the Yen starts to appreciate.

Segment 2: The Rupee-Yen Collision

When the Yen strengthens, the "Carry" trade works in reverse. A fund that borrowed Yen at ¥150/$ suddenly finds themselves owing money at ¥130/$. To repay the loan before it gets even more expensive, they must sell their most liquid, profitable assets.

In 2026, India is the most profitable asset in the emerging market basket.

Logic: FIIs (Foreign Institutional Investors) aren't selling Indian stocks because they've lost faith in India; they are selling because they need the cash to cover their Japanese margin calls.

Result: A coordinated sell-off in Mumbai that feels completely disconnected from domestic Indian earnings.

Segment 3: Why Small-Caps are the First to Bleed

While the Nifty 50 (Large Caps) often has the cushion of domestic institutional support (LIC, DIIs, Mutual Funds), the small and mid-cap segments are heavily influenced by Global Private Credit and Hedge Funds, the primary users of the Yen-Carry trade.

As Yen borrowing costs rise, the "overflow" liquidity that sustained 50x P/E ratios in small-caps vanishes overnight.

Segment 4: Carry Hangover Data Points

The End of the Free Lunch

The BoJ rate hike is a signal that the global floor for interest rates has moved. For the Indian investor, the Yen-Carry Hangover is a reminder that our markets do not exist in a vacuum. We are part of a global liquidity pool, and when the tap in Tokyo is turned off, the splash is felt in Mumbai.

The 2026 market isn't about Buying the Dip, it’s about Understanding the Plumbing. If the Carry Trade is unwinding, the era of easy alpha in speculative small-caps is over.