The Government Just Dropped Its Tax to 0%

If you want to understand just how seriously the government takes macro stability, stop looking at the equity markets and look at the extraordinary executive order that dropped on June 5.

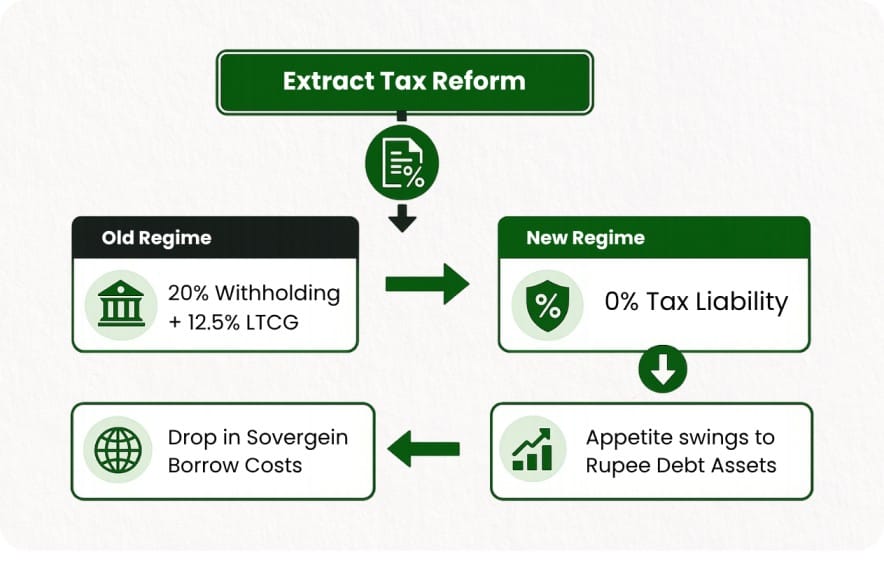

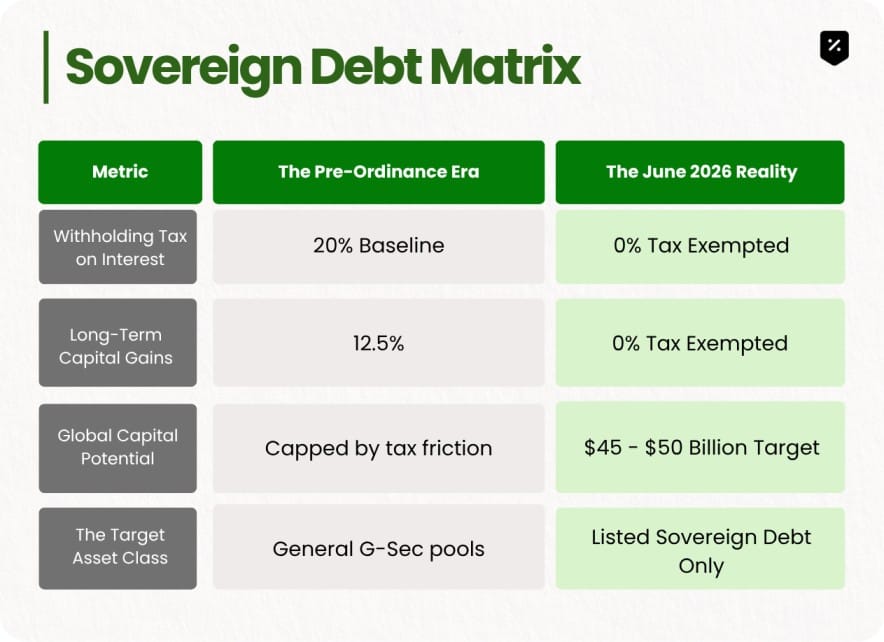

Through the Income-tax (Amendment) Ordinance, 2026, the Indian government completely wiped out taxes for foreign portfolio and institutional investors (FPIs/FIIs) holding sovereign government securities (G-Secs). Both the 12.5% Long-Term Capital Gains (LTCG) tax and the heavy 20% withholding tax on interest income have been reduced to an absolute zero.

And the government is in a hurry: the ordinance backdates this policy retrospectively to April 1, 2026.

This is not a minor bureaucratic tweak. This is an aggressive, coordinated emergency defence mechanism engineered to rewrite the financial plumbing of the Rupee and tap into trillions of dollars of global institutional capital.

In this edition, we’ll analyse:

- The Behind-the-Scenes Panic: The hidden currency mismatch that forced the Finance Ministry into an overnight executive decree.

- The Retrospective Arbitrage: The mathematical reality of what a zero-tax structure does to Indian bond yields on a global stage.

- The Global Index Catalyst: Why this zero-tax status paves the way for a $50 Billion institutional indexing tidal wave.

- The Domestic Risk-Reward: What happens to local corporate borrow yields when the sovereign market goes global.

Segment 1: The Hidden Currency Mismatch

On paper, India's economy is soaring, but the currency market has been fighting an invisible structural war.

Between late 2025 and March 2026, India’s actual balance of payments deficit sat at roughly $24 billion. Yet, the Reserve Bank of India had to aggressively pump $75 billion into the foreign exchange market just to steady the Rupee.

Why the massive discrepancy? Panic hedging. With crude oil hovering near uncomfortable baselines and FPIs aggressively pulling over $28 billion out of Indian equities this year, corporate importers and currency traders scrambled to buy dollars in advance, accelerating a downward spiral on the Rupee.

The government realized that trying to plug an equity-drain hole with verbal assurances wasn’t working. They needed a massive structural mechanism to build visible, predictable dollar inflows.

Segment 2: Breaking the Emerging Market Tax Stigma

India has historically been one of the very few emerging economies that strictly taxed foreign portfolio capital entering its sovereign debt market. This tax friction made Indian G-Secs structurally uncompetitive against peers like Brazil or South Africa, even though our underlying macro fundamentals were vastly superior.

By executing a double-strike removal of both withholding and capital gains taxes, the math of holding Indian sovereign paper flips instantly:

With an unencumbered gross-to-net yield profile, international funds can now capture the entire high-yield spread of Indian debt without factoring in dense domestic tax-compliance haircuts.

Segment 3: $50 Billion Indexing Accelerator

The macro game here is indexation. Passive global mega-funds track multi-trillion-dollar aggregates like the Bloomberg Global Aggregate and FTSE indices. Previously, the absolute operational and compliance friction of dealing with Indian tax registration kept thousands of global funds entirely on the sidelines.

With the tax barrier removed via executive decree, global asset managers can treat Indian sovereign bonds as standard, frictionless additions to global passive debt allocations. Industry leaders project that even a conservative 1% tracking inclusion rate shift across major global benchmarks translates to an automated $45 billion to $50 billion inflow into domestic debt markets over time.

The visibility of those incoming dollars acts as an instant psychological shock absorber for the local currency market, dampening the panic hedging that has plagued the Rupee all year.

The Bottom Line

When foreign institutions aggressively purchase Indian Government Securities, sovereign bond yields naturally compress because demand spikes. For the government, a lower bond yield means its gargantuan annual borrowing bill becomes drastically cheaper to finance—saving the national exchequer thousands of crores over the long haul.

For domestic equity and alternative asset allocators, the secondary effect is significant: as the sovereign yield curve flattens due to structural foreign capital buying, it resets the baseline cost of capital for the entire economy.

The government has chosen its defensive alignment. It is willing to sacrifice a sliver of immediate direct tax collection to secure a wall of institutional foreign exchange that keeps the broader financial ecosystem insulated from global shocks