The Devaluation of ₹1 Crore: Why India’s Favourite Retirement Number Just Broke

For a generation of Indian professionals, ₹1 crore was the ultimate retirement "magic number." It was the benchmark of success, whispered in insurance ads and brochures as the point where financial anxiety finally ends.

Here is the truth: The milestone didn't change, but the world did. As we step into 2026, ₹1 crore has transitioned from being a finish line to a mere checkpoint. Most people just haven't adjusted their math yet.

In this edition, we’ll talk about:

→ Part 1: How Much Has ₹1 Crore Actually Lost in Real Value?

→ Part 2: The Income Leap That Made ₹1 Crore Achievable

→ Part 3: The Housing Problem: Where ₹1 Crore Visibly Fell Apart

→ Part 4: The Healthcare costs nobody plans for

→ Part 5: Longevity Risk: The Math of Living Longer

→ Part 6: So What Is The New Number?

→ Part 7: The Psychological and Structural Shift

Part 1: How Much Has ₹1 Crore Actually Lost in Real Value?

This is where most people start the argument and stop too early. Yes, ₹1 crore in 2006 is not ₹1 crore in 2026. But the loss is far sharper than most people intuit.

Assuming a 6% annual inflation rate, which is conservative given India's actual trajectory. ₹1 crore today would be worth approximately ₹55.84 lakh after just ten years. Apply that backwards, ₹1 crore in 2006 had the purchasing power of roughly ₹3.2 - 3.5 crore in today's money, depending on the inflation measure you use.

But headline CPI understates the damage for the things that actually matter in retirement: housing, healthcare, and education. These three have inflated far faster than the general basket. If you weigh what an actual middle-class urban family spends on post-retirement healthcare, rent, travel, and lifestyle, the real devaluation is more severe than the standard inflation calculator suggests.

India's retail inflation for 2025 (January to December) averaged 2.25%, the lowest in years. But this recent low figure is deceptive in the retirement planning context. The relevant question is not what inflation is doing this year; it's what it has done over the twenty-year holding period of your wealth, and what it will do over the next twenty years of your retirement. On those timescales, the compounding is brutal.

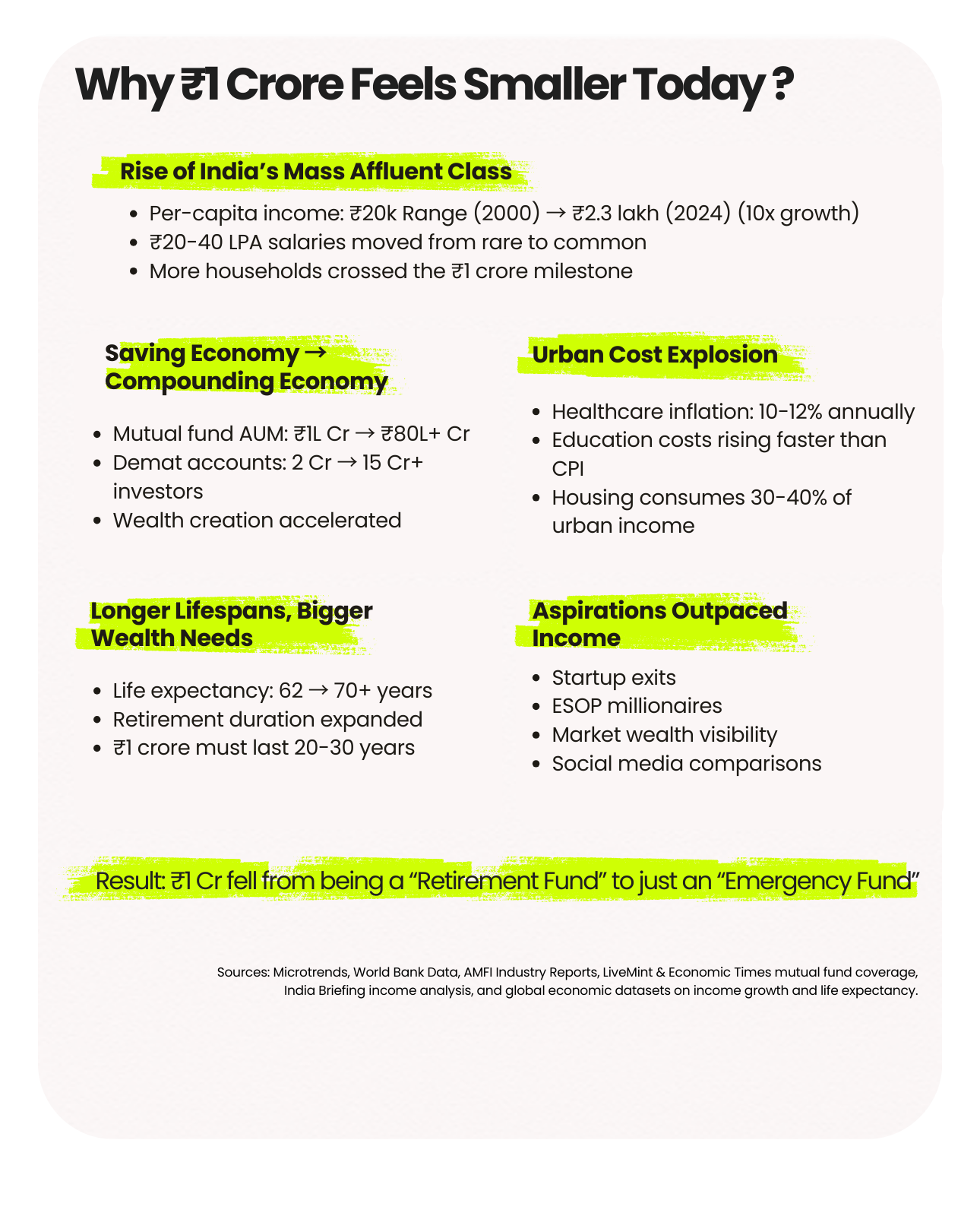

Part 2: The Income Leap That Made ₹1 Crore "Achievable"

The deeper story behind the devaluation of the crore milestone is that supply of crore-holders has exploded. When something becomes common, it loses status but more importantly for financial planning, it also stops being a reliable signal of long-term security.

India's per capita net national income was estimated at ₹1,88,892 in 2023-24, compared to roughly ₹20,000-25,000 range at the start of this century. That's close to an 8x nominal jump in per capita income in about twenty years. The professional class has grown even faster. Tech, finance, consulting, and startup ecosystems now routinely produce salaries of ₹20-40 LPA packages that were exceptional in 2005 but have become baseline expectations in certain sectors today.

Goldman Sachs Research estimates India's affluent consumer cohort, people defined by flying at least once a year, ordering food delivery monthly, and filing income taxes above ₹10 lakh will grow from around 60 million in 2023 to 100 million by 2027. A hundred million affluent people in one country. When the target audience for wealth is 100 million strong, the goalposts move. The crore milestone hasn't changed. The population capable of reaching it has exploded.

The wealth creation pipeline has industrialized too. India's mutual fund industry managed ₹81.01 lakh crore in AUM as of January 31, 2026, up from roughly ₹1 lakh crore two decades ago, with over 26.63 crore investor folios. Total demat accounts stood at 15 cr as of FY2026, growing from just 2 cr in March 2016.

The institutional scaffolding for building wealth has democratized entirely. SIPs, index funds, demat accounts with zero brokerage, the tools that once required a relationship manager at a private bank are now available to anyone with a smartphone. That acceleration shortens the timeline to ₹1 crore for millions of disciplined savers. Which means ₹1 crore stops being the destination and becomes an early checkpoint.

Part 3: The Housing Problem

Nothing illustrates the crore's devaluation more starkly than real estate.

In 2006, ₹1 crore could buy a legitimate flat in many large Indian cities, not a palatial one, but a reasonable 2BHK in a decent locality. Today, that same sum barely buys a studio in a mid-tier Mumbai suburb.

In Central Mumbai, even affordable localities have property rates starting around ₹17,000 - 22,000 per sq ft, while premium areas in South Mumbai exceed ₹46,000 per sq ft, with ultra-luxury zones like Malabar Hill and Marine Drive reaching above ₹1 lakh per sq ft. A modest 800 sq ft flat in Central Mumbai today costs ₹1.4 - 1.8 crore at minimum. In South Mumbai, you'd need ₹4 - 8 crore for anything remotely livable.

According to a JLL report, Mumbai and Delhi have seen house prices increase by around 10% per year over the past twenty years. At 10% compounded for 20 years, a ₹30 lakh flat in 2006 is worth over ₹2 crore today. The person who didn't buy that flat and saved the money instead is now trying to buy back into a market that has lapped them twice.

This is the first place where ₹1 crore shifts from the retirement fund to a down payment. In any Tier-1 Indian city, the housing equation alone can swallow a crore before you've even begun thinking about everything else.

Part 4: Healthcare: The Compounding Liability Nobody Prices In

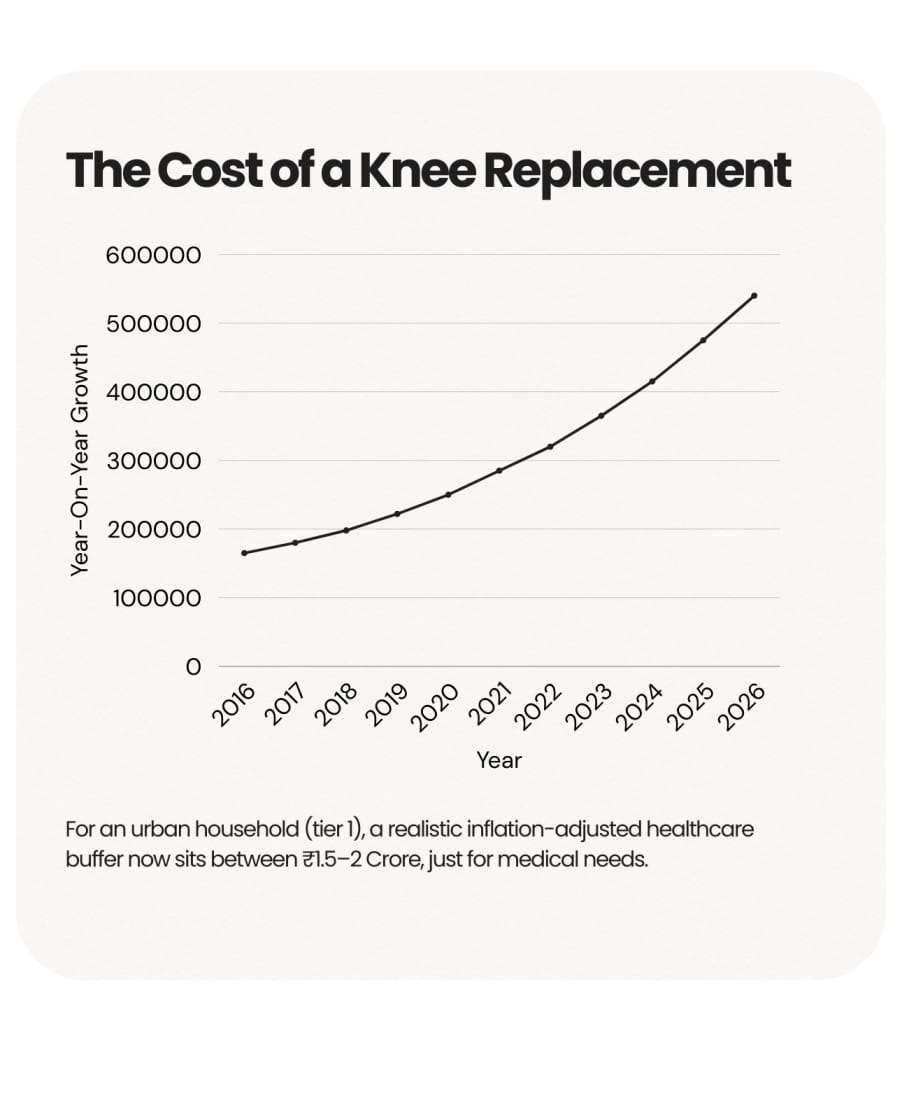

Of all the forces eroding the value of ₹1 crore, healthcare inflation is the most dangerous precisely because it's the one people least account for in their planning.

India's medical costs are rising at 11.5% to 14% annually, nearly three times the rate of general inflation. Medical inflation in India has averaged 10-12% per year over the past ten years, while general inflation has been around 5-6%, meaning healthcare costs are rising nearly twice as fast as income or savings.

The real-world impact is staggering. A knee replacement that cost ₹2.5 lakh in 2020 now runs closer to ₹4.2 lakh. A routine MRI went from ₹3,500 to ₹7,200. Medicines for chronic conditions diabetes, hypertension, and heart disease, are up 15% or more in five years. These are not exceptional medical events. They are the routine costs of aging.

Now project that forward. If healthcare inflation runs at 12% annually, costs double roughly every six years. Someone retiring at 60 and planning to live to 85 faces a 25-year healthcare liability window. The medical cost in their last decade of life will be 4-8 times what it is today. A crore earmarked entirely for healthcare would be depleted in a few serious hospital visits in that timeframe.

About 62% of all medical expenses in India are still paid directly by patients, not covered by insurance, and around 23% of families borrow money to pay hospital bills. Health insurance helps, but premiums are rising sharply: most private insurers raised premiums by 10-15% for the 2025-26 cycle, and moving into an older age band can spike your premium by 30-50%.

This is the factor that most destroys ₹1 crore as a retirement number. Healthcare inflation doesn't care about your savings rate. It compounds against you regardless.

Part 5: Longevity Risk: The Math of Living Longer

A crore stretched over 10 years is very different from a crore stretched over 30.

Life expectancy has risen significantly. Combined with better nutrition, urban healthcare access, and medical advances, many Indians today in their 40s and 50s are realistically planning for lifespans into their 80s and 90s. The retirement period has fundamentally changed.

Financial experts recommend planning for a retirement corpus to last until at least age 90 or 95. If you retire at 60, this means planning for 30 to 35 years of retirement. If your monthly expenses are ₹50,000 today, you'll need ₹1.45 lakh per month in 20 years. ₹1 crore will last less than 6 years. Read that again: ₹1 crore, at ₹50,000 monthly expenditure today, lasts under six years. For someone retiring at 60 with a 30-year horizon, ₹1 crore covers 20% of the retirement duration.

This is not a fringe case. It's the math for someone living in a Tier-2 city with modest but not austere expenses.

Part 6: So What Is The New Number?

This is where things get uncomfortable, because the honest answer is: it depends enormously on who you are and where you live, but for most urban Indians, the numbers are far higher than they expect.

Here's a practical framework using conservative assumptions (6% long-term inflation, 7-8% post-retirement returns, retirement at 60, lifespan to 85):

Tier-2 city, middle-class lifestyle (₹50,000/month current expenses): Using the 4% safe withdrawal rule, where you multiply monthly expenses by 300, your target retirement corpus works out to ₹1.5 crore at today's expense levels. But adjusted for inflation over a 20-year accumulation phase at 6%, that same lifestyle will cost ₹1.6 lakh per month at retirement, requiring a corpus of close to ₹5 crore.

Metro city professional (₹1 lakh/month current expenses): Planning for ₹50,000/month in today's terms as PERP (retirement expenses), inflation-adjusted at 7% over 20 years to retirement, with a 20-year post-retirement period and 10% corpus return, the base requirement is ₹5.1 crore and that's before adding a healthcare buffer (₹2+ crore in today's terms) and leisure provisions.

For early retirees or those with higher aspirations: The number climbs to ₹7 - 12 crore depending on lifestyle, city, and family obligations.

Financial planners increasingly recommend 30-40x annual expenses as a safer India-specific retirement rule, given our higher inflation, lack of robust social security, and longer family financial obligations.

The hard truth is this: for a family living comfortably (not lavishly) in urban India today, a genuine retirement corpus is somewhere between ₹5 crore and ₹10 crore, depending on the city, health, lifestyle expectations, and age of retirement. ₹1 crore barely serves as an emergency buffer for such a family.

Part 7: The Psychological and Structural Shift

Beyond the numbers, something subtler has changed in how Indians perceive and pursue wealth.

The post that inspired this was right that aspiration inflation has accelerated faster than income growth. Social media has given everyone a window into startup exits, ESOP millionaires, and visible wealth creation at a scale that earlier generations didn't see up close. When your reference class is people who made ₹5 crore from stock options at 35, ₹1 crore starts to feel like a rounding error, not because it actually is, but because the psychological benchmark has shifted.

A phrase now often heard in investment circles is "financial assets are the new gold," capturing how the younger generation is prioritizing stocks and funds over the traditional rush to buy gold or property. This is a genuinely healthy shift, but it also means more people are exposed to market volatility, and the difference between good and bad asset allocation over a 30-year horizon can be the difference between financial security and crisis.

The deeper structural point: retail investors lost close to ₹3 lakh crore in derivatives trading between FY22 and FY25, with SEBI estimating that 91% of retail derivatives traders lost money. Access without financial education is dangerous. The democratisation of investing has created both real wealth and real destruction, often for the same people.

The Real Takeaway

₹1 crore in 2026 is not worthless. For a single person in a Tier-3 city living frugally, it can still provide a meaningful cushion. But for the urban professional who built it as a retirement goal over fifteen years of careful saving, it is a starting point, not a finish line.

The more honest framing of the post's question, "What's the new number?" is that there is no single new number. The correct number is a function of:

- Your city and lifestyle (metros need 2-3x what Tier-2 needs)

- Your health baseline (a family with a chronic disease history needs a significantly larger healthcare buffer)

- Your retirement age (every five years earlier roughly doubles the corpus needed)

- Your income replacement needs (the 4% rule means ₹1 lakh/month lifestyle needs ₹3 crore minimum; ₹2 lakh/month needs ₹6 crore)

- Your allocation quality (the same corpus invested in FDs vs. equity mutual funds can produce 40–50% different outcomes over 20 years)

The era when hard work plus savings equaled security is over. Hard work plus smart allocation might. Hard work plus poor allocation almost certainly won't, because inflation is not neutral; it compounds against you as reliably as markets compound for you.

The new number for a comfortable urban Indian retirement is not a crore. It's almost certainly a multiple of five. And for anyone in a Tier-1 metro with aspirations beyond bare subsistence, it's a multiple of ten.