The ₹2,000 Note Withdrawal: Did It Actually Change Anything?

When the RBI announced the withdrawal of the ₹2,000 denomination in May 2023, the ghosts of 2016’s demonetisation immediately resurfaced. However, the 2023 exercise was fundamentally different: it was a withdrawal from circulation rather than an overnight ban. Now, with the benefit of hindsight in 2026, we can ask the hard question: Did it actually change the plumbing of the Indian economy, or was it just an administrative cleanup of a note that had already lost its utility?

In this edition, we’ll cover:

- The Liquidity Surge: How the return of dead cash temporarily flushed the banking system.

- The Digital Transition: Why the withdrawal accelerated the final push toward UPI for high-value retail.

- The Black Money Myth: Did the withdrawal actually catch unaccounted wealth, or just shift its form?

- Currency Management: The transition back to a ₹500-dominant economy.

Segment 1: Systemic Liquidity Flush

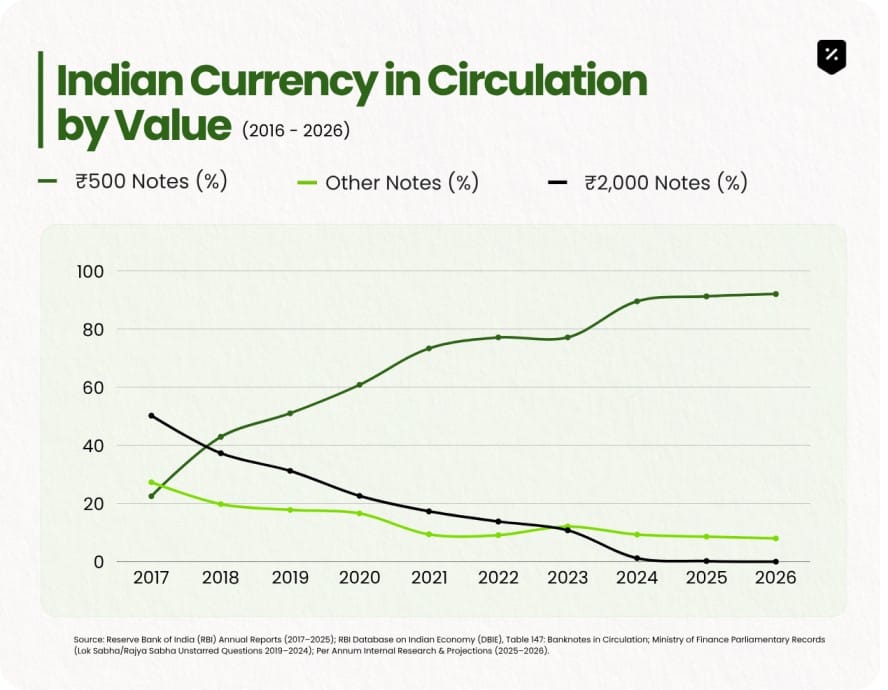

One of the most immediate impacts was the massive influx of deposits into the banking system. As of the final windows, over 97% of the ₹3.56 lakh crore in ₹2,000 notes had returned to the banks.

For a brief period, this created a significant Liquidity Surplus. Banks, which were struggling with high Credit-to-Deposit (CD) ratios, suddenly found themselves with a cheap source of CASA (Current Account Savings Account) funds. However, this was a transient sugar high, much of this liquidity was eventually absorbed by the RBI through Variable Rate Reverse Repo (VRRR) auctions to prevent a spike in inflation.

Segment 2: The "Digital-First" Retail ShiftThe ₹2,000 note was always an awkward denomination for daily use. Its withdrawal coincided with the massive scale-up of Credit on UPI. By removing the highest denomination of cash, the friction of making high-value purchases (₹5,000 - ₹20,000) in cash increased. This pushed the captive Class and merchants alike to formalise transactions. In 2026, we see the result: UPI penetration in the Mid-Ticket segment has tripled since the withdrawal announcement, as the hassle of carrying bundles of ₹500 notes outweighed the perceived anonymity of cash.

Segment 3: Black Money Paradox

The skeptics argue that the withdrawal did little to curb the shadow economy. Unlike 2016, there was no massive extinguishment of currency.

- Velocity Factor: Instead of letting the notes sit dead in lockers, the withdrawal forced the velocity of money to increase.

- Luxury Pivot: We saw a massive, localized spike in gold and luxury watch sales during the exchange window, a classic Hard Asset hedge for those looking to convert cash without entering the banking ledger.

- Result: The move didn't eliminate unaccounted wealth; it simply forced it to migrate from paper into Hard Collectibles or Real Estate premiums (as we’ve seen in the Gurgaon rental spikes).

Segment 4: The Return to a "₹500 Economy"

Today, the ₹500 note accounts for the vast majority of the value of currency in circulation. This has created a Currency Management challenge.

The reliance on a single high-value denomination (₹500) makes the economy more susceptible to counterfeiting risks and logistical bottlenecks in ATM replenishment.

The Quiet Success of Nudging

The ₹2,000 note withdrawal wasn't a shock to the system; it was a surgical nudge. It successfully retired a denomination that had become a tool for hoarding, without the catastrophic supply-chain disruptions of 2016.

However, it also exposed a structural truth about the Indian economy: Cash isn't going away; it's just getting smaller. While we celebrate the digital boom, the ₹500 Economy remains the bedrock of India's informal trade. The withdrawal changed the face of our wallets, but the nature of our shadow economy remains as resilient as ever.