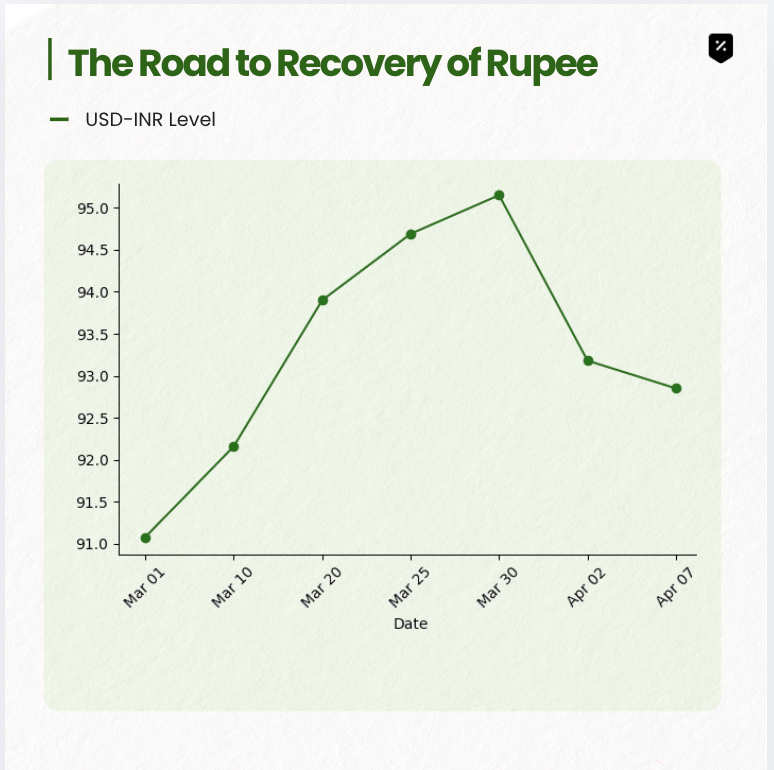

Rupee Rebounds to 92.85: Is RBI Finally Stabilising the INR?

The Indian Rupee staged a firm 33-paise recovery in early trade on April 6th and has managed to hold those gains into this morning, April 7th, trading near 92.85. While this provides a tactical window of stability, it comes at a time when Brent crude has surged to $111.20 following a heightened Tuesday Deadline from Washington regarding the Strait of Hormuz.

The recovery is not a reflection of cooling oil prices. Instead, it is a structural squeeze engineered by the Reserve Bank of India (RBI) to decouple the Rupee from the predatory Energy-Currency Loop.

In this edition, we analyse:

- The $100 Million Cap: Deconstructing the RBI’s clampdown on bank positions.

- The NDF Plug: How offshore speculation was neutralized in a 48-hour window.

- The $30.5 Billion Drawdown: Evaluating the cost of defending the ₹93 floor.

- The Investment Playbook: Navigating the "Managed Float" during a geopolitical stalemate.

Section 1: The Speculation Squeeze

The recovery was driven by the RBI’s surgical strike on the Non-Deliverable Forward (NDF) market. Speculators had been using offshore instruments to bet against the Rupee, creating a downward spiral that the domestic spot market was forced to follow.

The Structural Intervention:

- Net Open Position (NOP) Enforcement: The RBI has strictly capped banks' net open positions at $100 million. This forced institutional desks to unwind Long Dollar positions, creating immediate artificial demand for the Rupee.

- The Liquidity Drain: By restricting banks from offering NDF contracts to residents, the RBI effectively plugged the leak that was draining domestic liquidity into offshore speculative bets.

Section 2: The Cost of Defense

Defending the Rupee is a war of attrition. To maintain the 92-93 range, the RBI has deployed its War Chest at an unprecedented rate.

- The Monthly Plunge: India’s Forex reserves saw their steepest decline in the 2020s, falling by $30.5 Billion in March to end at $688.1 Billion.

- The Forward Book Risk: To protect physical spot reserves, the RBI has increased its net short position in the forward market, estimated now at $100 Billion. This creates a future dollar liability that must be settled when these contracts mature.

Professional Insight: While 11 months of import cover remains on paper, the Effective Cover adjusted for forward liabilities is closer to 8.5 months. The RBI is buying time for a geopolitical resolution in the Strait of Hormuz.

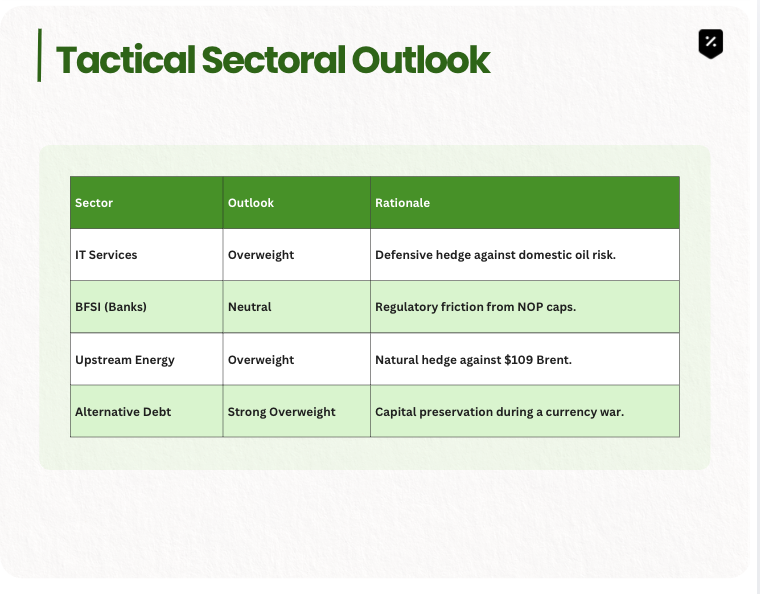

Section 3: Sectoral Divergence

A rebounding Rupee creates a brief arbitrage window for specific sectors while placing others under regulatory stress.

- IT Services: While a stronger Rupee technically hits margins, the sector acts as a Safe Haven for FIIs looking to stay in India without being exposed to high-oil-consuming manufacturing.

- BFSI (Banks): The biggest losers of today's recovery are actually the banks. The $100M NOP cap limits their ability to profit from currency volatility, leading to a temporary contraction in treasury income.

- Automobiles: Despite the Rupee's 33-paise gain, the sector remains Underweight as long as Brent stays above $105, as fuel-led demand destruction outweighs currency benefits.

Conclusion

The 33-paise rebound is a symptom of technical intervention, not fundamental recovery. As long as the Strait of Hormuz remains a chokepoint and Brent crude touches $111, the Rupee exists in a state of Managed Fragility.