How GCCs Just Hijacked 48% of India’s Prime Real Estate.

We have been waiting for this tectonic shift. For years, India’s office market has grown steadily, but Q1 2026 marked a fundamental structural inversion. Global Capability Centres (GCCs); the strategic, innovation-led hubs of global multinationals, now capture a staggering 48% of total leasing activity across India's top cities.

This isn’t about cost arbitrage anymore; it is about core enterprise capabilities. India has transitioned from being the world’s back-office to becoming its strategic nerve center. The defining signature of the next decade of Indian wealth creation is the shift from servicing the world to owning its innovation ecosystem.

In this edition, we will cover:

- The 48% Structural Inversion: How Global Capability Centers (GCCs) officially became the primary driver of Indian office demand, leapfrogging traditional IT services.

- Beyond the Back-Office: Why BFSI, Healthcare, and Engineering giants are moving their core R&D and decision-making platforms to India.

- The Grade-A Gridlock: A deep dive into the supply-demand mismatch forcing MNCs to pre-lease space 36 months in advance.

- Permanence vs. Churn: An investor’s map of high-resilience clusters (like Whitefield and Hitech City) versus high-risk peripheral hubs.

- The Economic Multiplier: How the rise of high-income GCC leadership is fundamentally premiumising nearby residential and retail ecosystems.

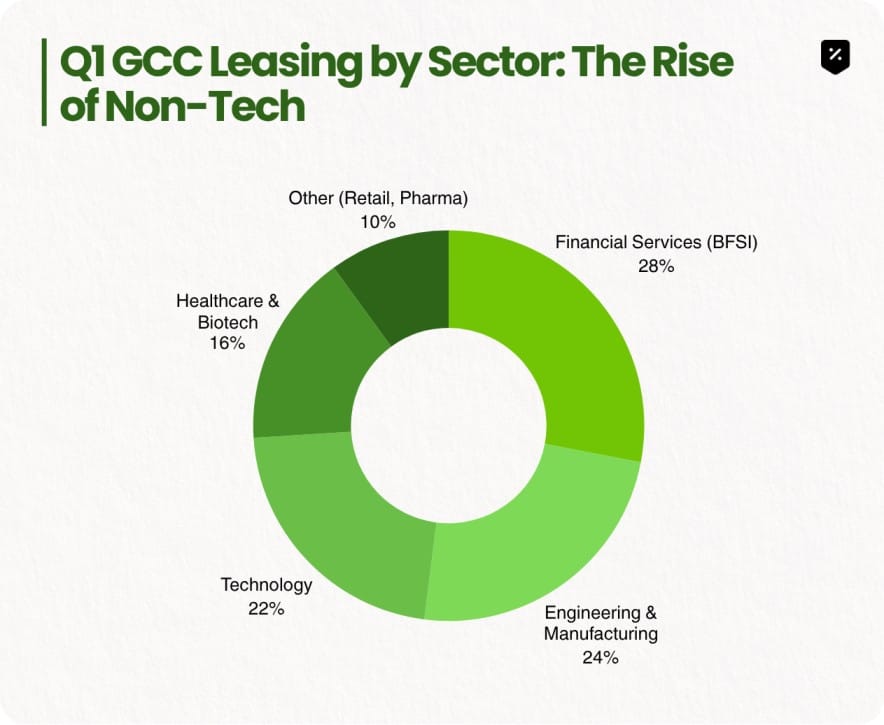

Segment 1: Sectoral Inversion (Beyond technology)

If you are only analysing technology firm leasing, you are missing the acceleration. The GCC story in 2026 is defined by diversification.

Engineering & Manufacturing, Financial Services (BFSI), and Healthcare giants are transitioning their India-based centers from peripheral delivery units to decision-making platforms. They are building advanced data analytics, AI risk models, and core product design hubs.

This means that while traditional IT services may moderate, the GCC base is structurally widening, making their real estate footprints exceptionally resilient.

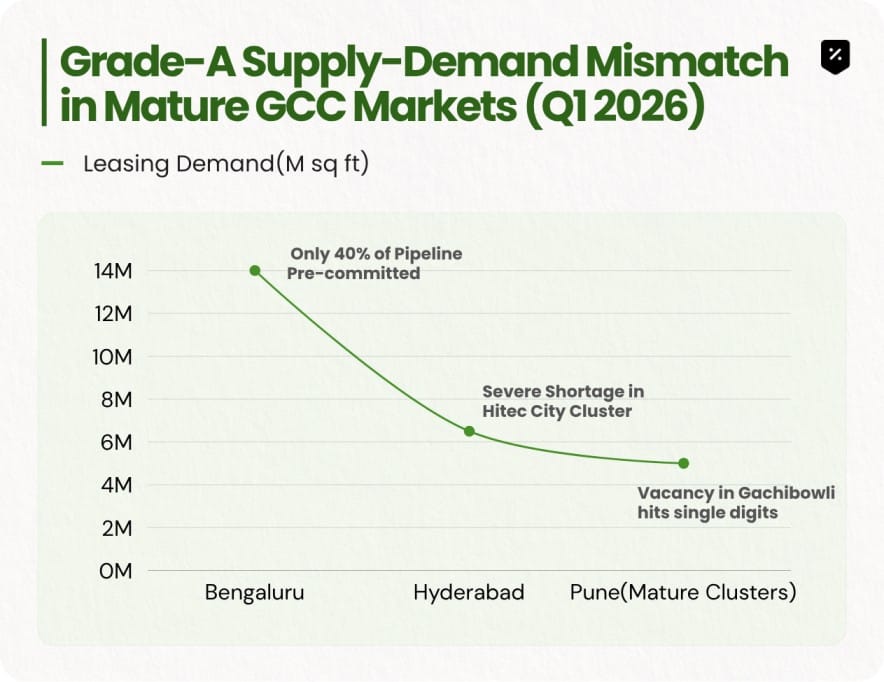

Segment 2: The Infrastructure Wedge (Quality over Quantity)

The most exciting, and for some concerning trend we are watching is that this GCC demand is colliding with a severe Grade-A supply bottleneck.

Hybrid work did not kill the office; it made ESG-compliant, technology-intensive Grade-A space mandatory. GCCs are refusing anything that is not premium quality.

This supply gridlock is driving pre-commitments, with many GCCs forced to lock-in space 24-36 months in advance just to secure their growth pipeline. Pre-commitments are the ultimate signature of long-term permanence.

Segment 3: Campus Permanence versus Occupier Churn

For the commercial real estate investor, the defining challenge of 2026 is distinguishing Campus Permanence from Occupier Churn.

Where complexity resides, capital becomes permanent. Peripheral hubs built for low-complexity mandates remain vulnerable to global churn. Micro-markets like Whitefield and ORR (Bengaluru), and Hitec City (Hyderabad) have evolved from tech parks to concentrated ecosystems of specific human talent, which guarantees long-term resilience