Hormuz & The Rupee: The Macro-Mechanics of an Oil Shock.

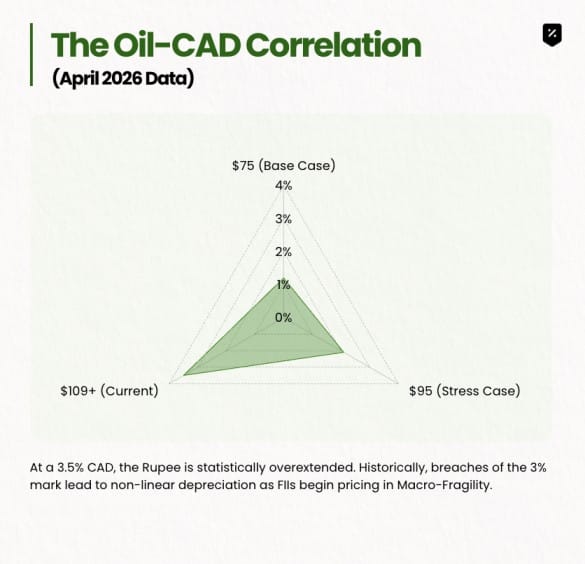

As of this morning, Brent crude is trading at $109.03, driven by the physical blockade of the Strait of Hormuz, the artery for 21% of global seaborne oil. For India, this isn't just a fuel spike. It is a structural assault on the Current Account Deficit (CAD), a threat to the ₹94.59 Rupee, and a direct tax on corporate margins.

The buffer is gone. With the Rupee touching a record intra-day low of ₹95.21 this week, we are entering a Currency-Energy feedback loop. When Brent jumps while the Rupee slides, the cost of a barrel for India doesn't just rise, it compounds.

In this edition, we analyse:

- The $21.4B Monthly Drain: Slicing the Current Account Deficit (CAD) with surgical precision.

- The Logistics Multiplier: Why the "Cape of Good Hope" rerouting is a hidden tax on Indian SMEs.

- The Sectoral "Red Zones": Identifying the 500 bps margin contraction in India’s industrial heavyweights.

- The 2026 Investment Playbook: A data-backed framework for navigating a market where the Equity Risk Premium has turned negative.

Section 1: The Macro-Drain (CAD & Currency)

India imports 85-87% of its crude oil, making it one of the most energy-sensitive economies in the G20. The current disruption in the Strait of Hormuz has moved India from a "comfortable growth" phase into a "defensive macro" phase.

Forex Intervention Trap:

The RBI has historically maintained a shield of $600B+ in reserves. However, defending a currency against a structural energy blockade is an expensive war of attrition. To keep the Rupee from spiraling toward ₹100, the RBI is estimated to be selling $1.5 Billion to $2 Billion weekly. This reduces India's Import Cover, the number of months of imports the country can sustain, placing downward pressure on India’s sovereign credit outlook.

Inelastic Demand Problem:

Unlike luxury goods, India cannot simply stop importing oil. Our transport, agriculture, and industrial sectors are hard-coded to diesel and petrol. This means as prices rise, the volume stays constant, leading to a massive, non-negotiable dollar outflow.

Section 2: The Logistics Multiplier

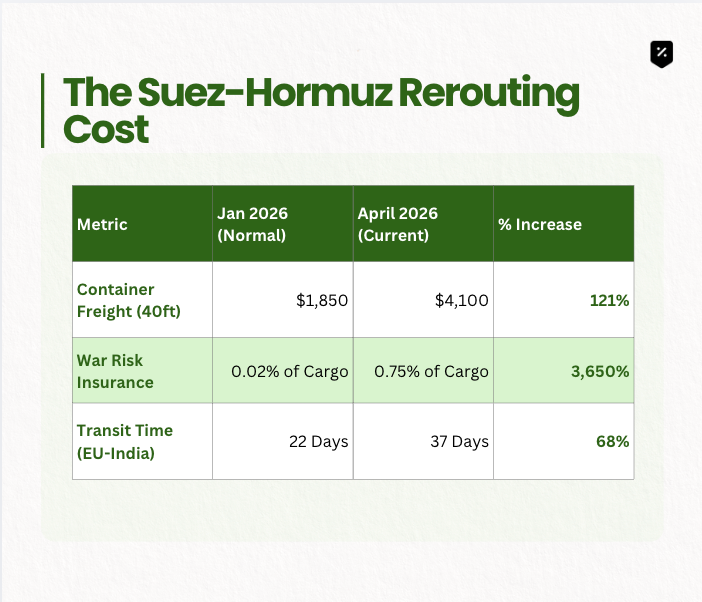

Beyond the pump price, the Hormuz blockade has fundamentally broken the "Just-in-Time" supply chain for Indian manufacturers.

The Cape of Good Hope Tax Shipping giants MSC and Maersk have rerouted virtually all Asia-Europe traffic around the southern tip of Africa. This adds 6,500 kilometers and 15 days to every voyage. For an Indian SME in the auto-component or textile space, this delay is catastrophic for two reasons:

- The Interest Trap: Most Indian exporters operate on Export Bill Discounting (EBD). An extra 15 days of transit means 15 days of additional interest paid to the bank before the payment is released by the overseas buyer.

- Container Scarcity: Because ships are taking longer to return, there is a physical shortage of empty containers at Mundra and Nhava Sheva ports, driving "spot" freight rates up by 121%

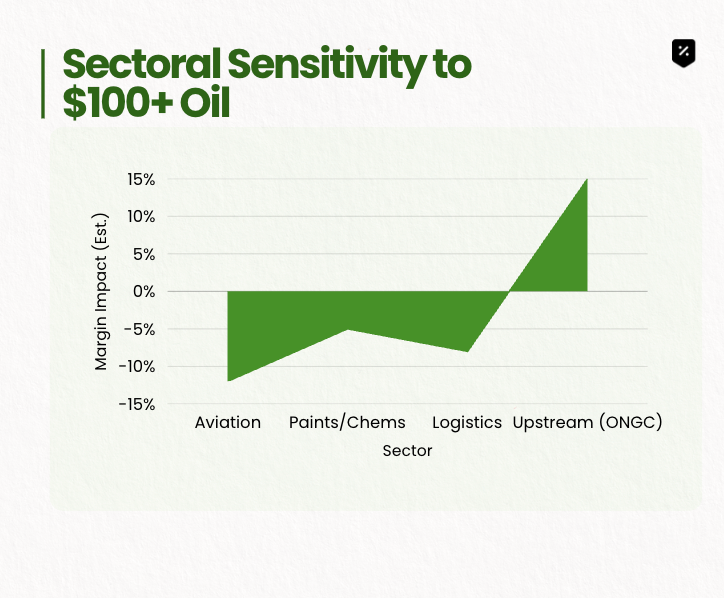

Section 3: Sectoral Red Zones

We are moving from Demand-Pull inflation to Cost-Push inflation. Companies can no longer pass on these costs to an already-stretched Indian consumer.

Petrochemical Ripple Effect

Sectors like Paints, Adhesives, and Plastics use crude oil derivatives as 50-60% of their raw material stack. With oil at $109 and the Rupee at 94.5, their Input Tax has effectively risen by 43% since January.

- Aviation: Air Turbine Fuel (ATF) pricing is revised fortnightly. With the Rupee's collapse, airlines are seeing their single largest expense (priced in USD) explode while their revenue (tickets) is in weaker INR.

- Agriculture: India’s winter crop (Rabi) harvesting and summer crop (Zaid) sowing are diesel-intensive. High fuel costs act as a regressive tax on rural India, dampening FMCG demand for the next two quarters.

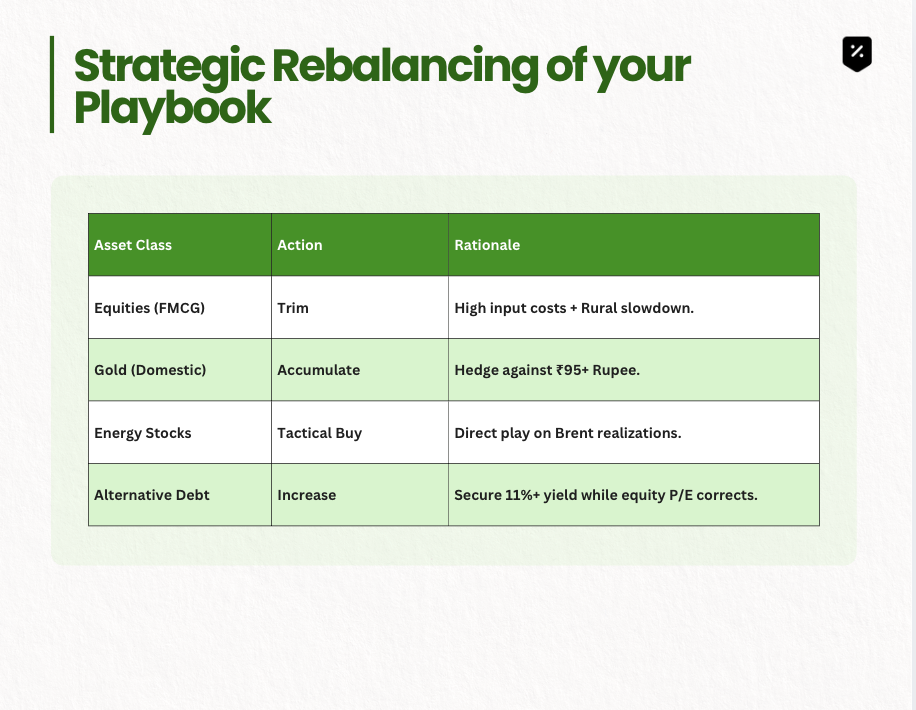

Section 4: The 2026 Investment Playbook

In an environment where the Equity Risk Premium (ERP) has turned negative, meaning you aren't being compensated for the risk of holding stocks vs. safe bonds, the strategy must shift to Capital Preservation.

1. Gold as the Currency Arbitrage

Gold is priced globally in Dollars. When the Rupee falls from 83 to 94.5, the domestic price of Gold rises even if the international price stays flat. This makes Gold the most efficient hedge against the RBI's inability to defend the Rupee.

2. The Alternative Debt Pivot

With equity multiples (P/E) likely to compress as earnings are downgraded, the yield on stocks is falling. High-Yield Alternative Debt (11-12%) currently offers a Real Return (Yield minus Inflation) that is 400 bps higher than the Nifty’s earnings yield.

The 2026 Oil Shock is not a "v-shaped" event. The physical blockade of Hormuz is a geopolitical stalemate. At $109 Brent and ₹94.59 INR, your portfolio isn't just fighting inflation, it's fighting a structural energy blockade.