Are Pre-Leased Bank Properties Still Safe?

If you have a parent approaching retirement or if you manage family wealth, you’ve almost certainly seen the pitch. A real estate broker calls with a bulletproof asset: a commercial ground-floor lock-up shop pre-leased to a major private or public sector bank.

The brochure promises an investment that runs on autopilot. You get an immediate 8% to 9% rental yield, a AAA-rated institutional tenant, a 9-year lease contract, and zero property management headaches. For an individual looking for steady cash flow to replace their salary, it looks like the ultimate safe haven.

But behind the slick presentations, a quiet structural shift is happening in retail property development. Banks are quietly breaking their long-term lease lock-ins, packing up their physical branches, and leaving retail investors stranded with highly inflated, empty properties that are nearly impossible to re-lease at the same premium.

Here is the data-backed reality of how banking automation is colliding with retail real estate.

In this edition, we’ll analyse:

- The Artificial Premium: How developers manipulate rental yields to inflate the sale price of commercial shops.

- The Digital Migration Data: The raw numbers driving the closure of physical bank branches across urban India.

- The Lock-In Illusion: Why a 9-year corporate lease agreement offers virtually zero protection to a retail landlord.

- The Re-Rating Risk: The brutal math of trying to find a new tenant when a bank walks out.

Segment 1: The Math of the Illusion

To understand why this trap works so well, you have to look at how developers manufacture these deals.

Imagine a commercial retail space that has a true market rental value of ₹1.5 Lakh per month. A developer looking to unload this property will approach a bank and offer them an aggressively subsidised rent; say, ₹1 Lakh per month, if they sign a long-term lease agreement.

Simultaneously, the developer approaches a retail buyer and pitches the property based on an artificially high expected rental yield. They sell the property at a premium valuation based on the security of the bank tenant. The moment the property is sold, the developer walks away with a massive capital gain, leaving the buyer holding an asset whose valuation is tied entirely to a tenant that has no intention of staying for a decade.

Segment 2. The Digital Migration

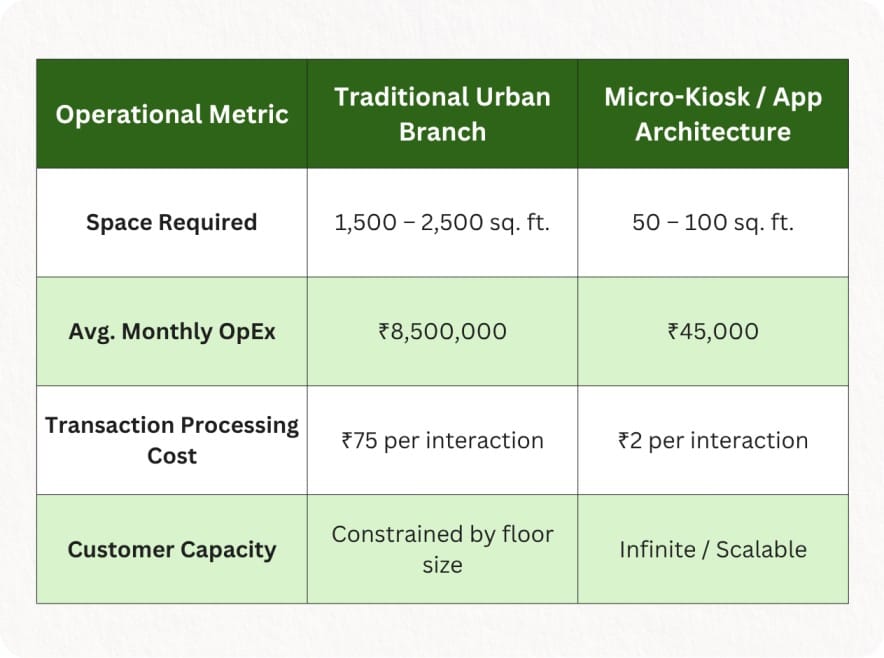

Physical bank branches are facing an existential crisis. The cost of maintaining a traditional brick-and-mortar branch in a Tier-1 metro now averages ₹6 Lakh to ₹12 Lakh per month in pure operational expenditure (rent, security, electricity, air conditioning, and on-site staff).

Meanwhile, the transactional volume inside these physical branches has plummeted.

According to recent retail banking performance metrics, over 88% of all savings account operations, fixed deposit creations, and personal loan disbursements are now processed entirely via mobile apps. For everything else, banks are deploying automated micro-ATMs and self-service kiosks that require less than 100 square feet of space.

The financial incentive for banks to downsize is overwhelming. They do not need your 2,000-square-foot ground-floor corner property anymore.

Segment 3: The Lock-In Illusion

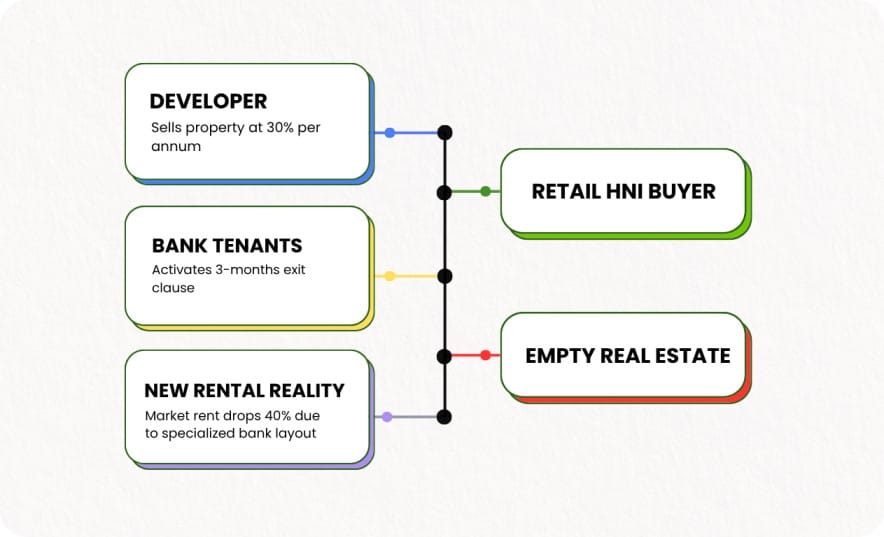

When an investor points out the 9-year lease agreement, brokers point to the 3-year lock-in period clause as a iron-clad guarantee. This is a fundamental misunderstanding of corporate legal power.

In a standard commercial lease drafted by a bank’s institutional legal team, the clauses are heavily weighted in favor of the tenant. While the landlord is locked in and cannot evict the bank, the bank almost always retains a exit clause allowing them to vacate the property by serving a basic 3 to 6-month notice period, even during the lock-in window, by paying a nominal penalty.

When a bank decides a branch is unviable due to localised digital adoption, they do not hesitate to trigger this clause, pay the minor penalty, and walk away.

Segment 4: The Capital Damage

When a bank vacates, the retail investor isn't just losing a tenant; they are losing their capital valuation.

Bank branches are highly customised spaces. They feature reinforced concrete strongrooms, heavy locker vaults, extensive internal partitioning, and specialised electrical wiring. Stripping a former bank property back to a raw, leasable commercial shell can cost a landlord anywhere from ₹5 Lakh to ₹15 Lakh.

Furthermore, finding a tenant who can match the rental premium a bank used to pay is incredibly difficult. Restaurants, apparel stores, and local businesses cannot afford the high per-square-foot rates that financial institutions once paid for security and visibility. Landlords are frequently forced to accept a 30% to 50% haircut on rent just to keep the property from sitting empty.

The Strategy Moving Forward

If you are evaluating commercial real estate for passive income, stop buying the brand name on the lease document.

- Test the Baseline Rent: Strip the bank tenant away from the equation. If the bank left tomorrow, could a local apparel brand or an upscale cafe afford to pay the exact same rent? If the answer is no, the property is dangerously overvalued.

- Audit the Exit Terms: Never accept a generic corporate lease draft. Insist on symmetric lock-in penalties where the tenant must pay out the remaining lease value if they exit prematurely.

- Look at Infrastructure Over Brand: Premium logistics hubs, micro-warehouses, and grade-A medical diagnostic spaces are facing structural demand growth. Brick-and-mortar retail banking, on the other hand, is a shrinking footprint.

Don't let the comfort of a corporate logo blind you to the reality of the digital balance sheet.