Are Indian Equities Worth the Premium?

Introduction: Nifty at 24,000 - Triumph or Trap?

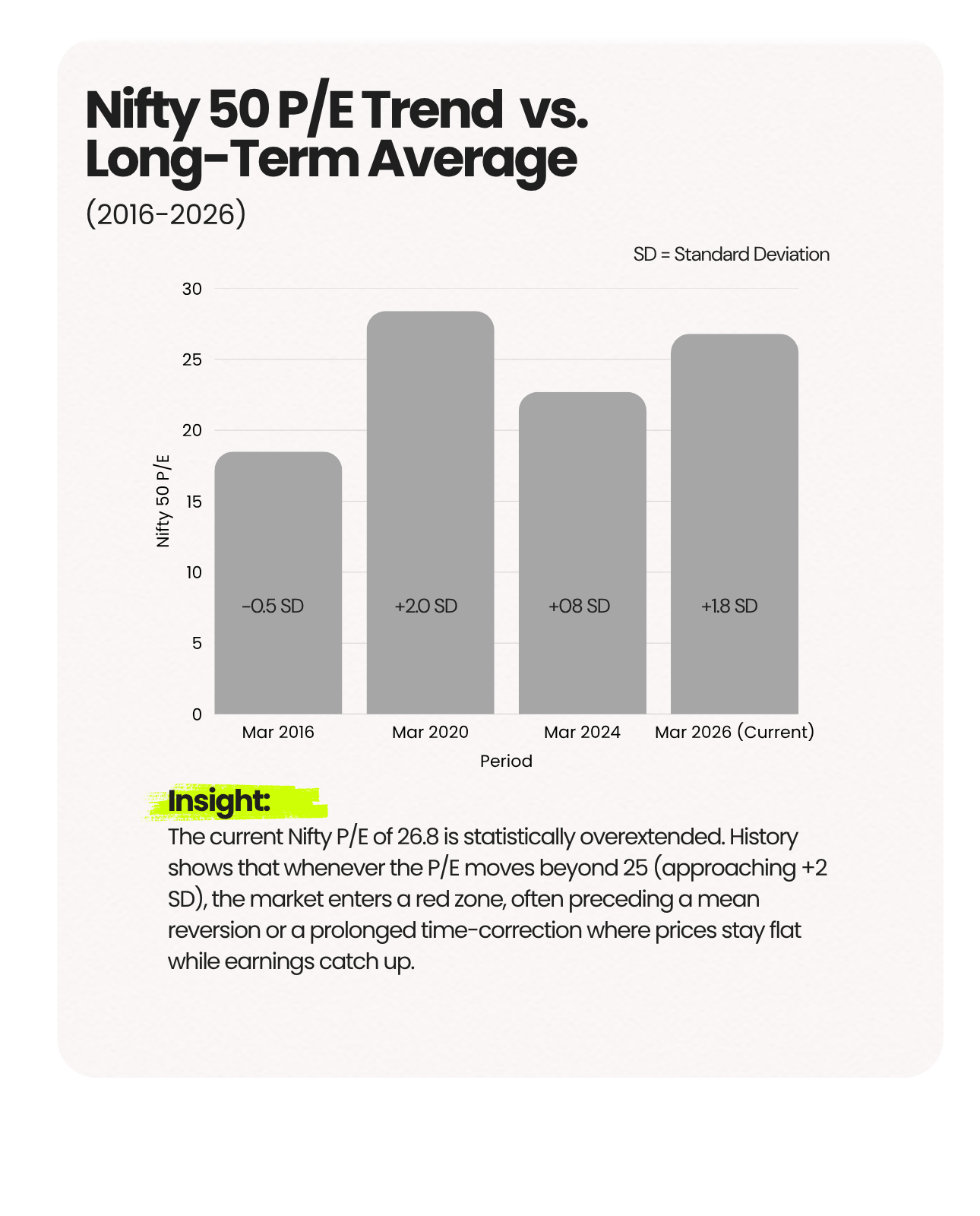

The headline numbers are undeniable: The Nifty 50 is hovering around the 24,000 mark, a staggering 220% climb from its March 2016 lows. To any global investor, this looks like a resounding success story. Yet, as we move through March 20, 2026, a quieter, more contentious debate is taking place on trading desks across Mumbai.

Are these premiums justified?

India has long been known as an expensive market, trading at a significant premium to its emerging market peers. But with a price-to-earnings (P/E) ratio that is currently more than one standard deviation above its long-term average, the consensus is fraying.

In this edition, we’ll talk about:

- The Valuation Question: A post-mortem of the factors that have driven India's P/E to its current level.

- The Earnings Reality Check: Slicing through the headline numbers to see if real corporate profits are keeping pace.

- The Sectoral Divergence: Identifying the pockets of true value versus the ones that are merely expensive.

- The Investment Playbook: A data-backed framework for navigating a market priced for perfection.

Today’s deep dive is not just about valuation metrics; it is a factual investigation into whether India's economic fundamentals can support its stock market’s ambitious pricing.

Section 1: Slicing the P/E – The High Cost of Investing in India

The standard P/E ratio is the market's primary scorecard. A high P/E implies that investors are willing to pay more for every rupee of earnings. In India, this willingness has reached historic highs due to a unique blend of structural and qualitative factors.

The "Quality" Premium

Unlike many emerging markets heavily dependent on commodity cycles (Brazil) or geopolitical volatility (China), India has built a reputation for high-quality, domestic-consumption-driven earnings. This certainty commands a premium.

The Structural Shift

We are witnessing a structural rerating. Factors such as the digitalization of the economy (DPI), the shift to organized retail, and the ₹30,000 Crore monthly SIP inflows have created a persistent domestic bid for stocks, providing a floor to valuations even when global sentiment is shaky.

Section 2: The Reality of Earnings (Are Profits Real?)

A high P/E is only sustainable if earnings are explosive. In the bullish scenario, the current 26.8x multiple is simply pricing in a massive jump in future profits. But is the core business delivering?

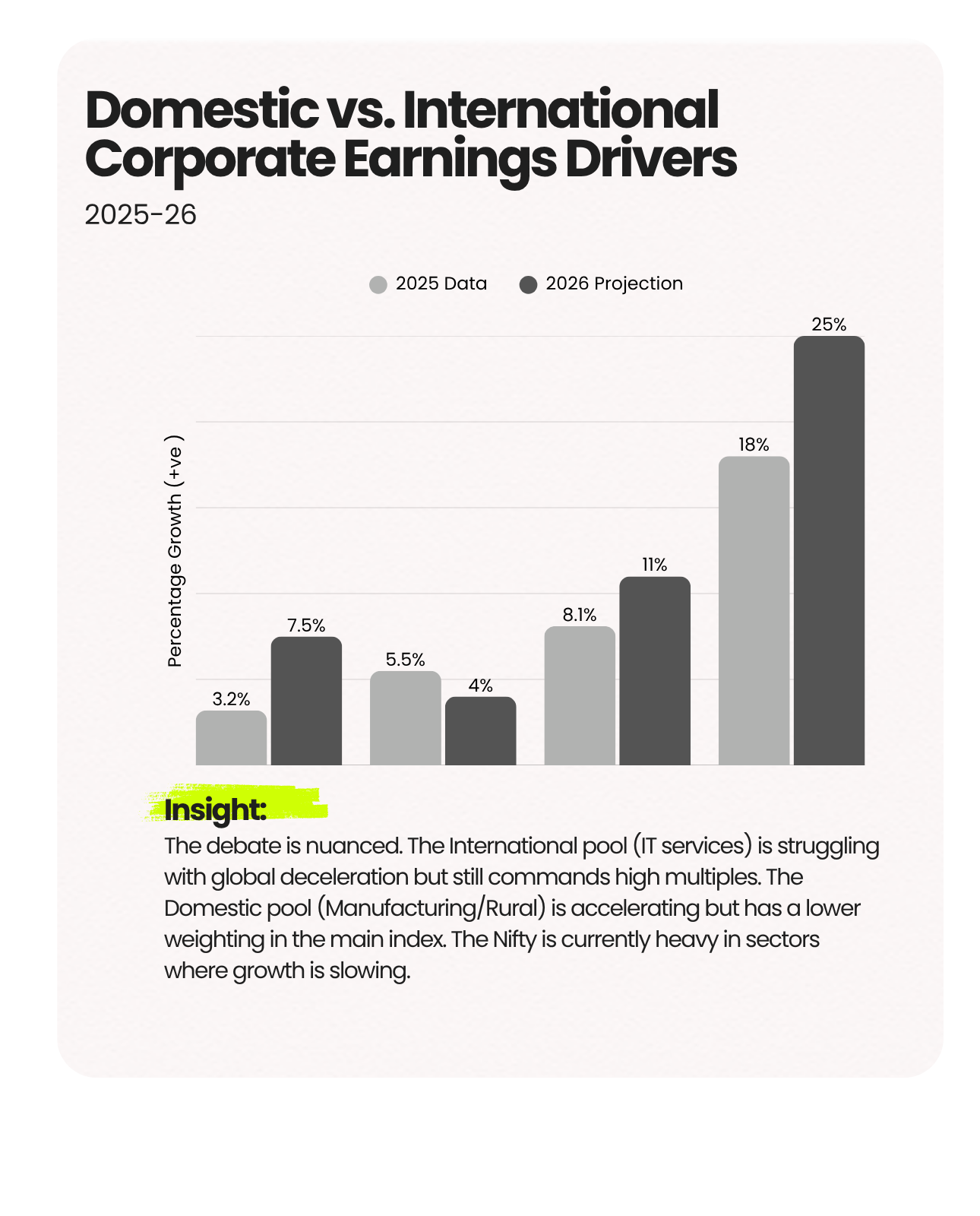

Headline EPS vs. Core Earnings

The Nifty 50 EPS has grown by 14% YoY in 2025-26. On the surface, this is robust. However, a deeper audit reveals a widening gap. A significant portion of this growth came from Other Income (treasury gains from high interest rates) and one-off divestments.

Core Operating Profit growth (EBITDA) was closer to 9.5%.

This creates an earnings gap where the price multiple is expanding faster than the actual operational ability of companies to generate surplus cash.

Section 3: Where is the Real Value?

In 2026, the market is not a monolith. It is a tale of two valuation regimes.

The Overcrowded Trades

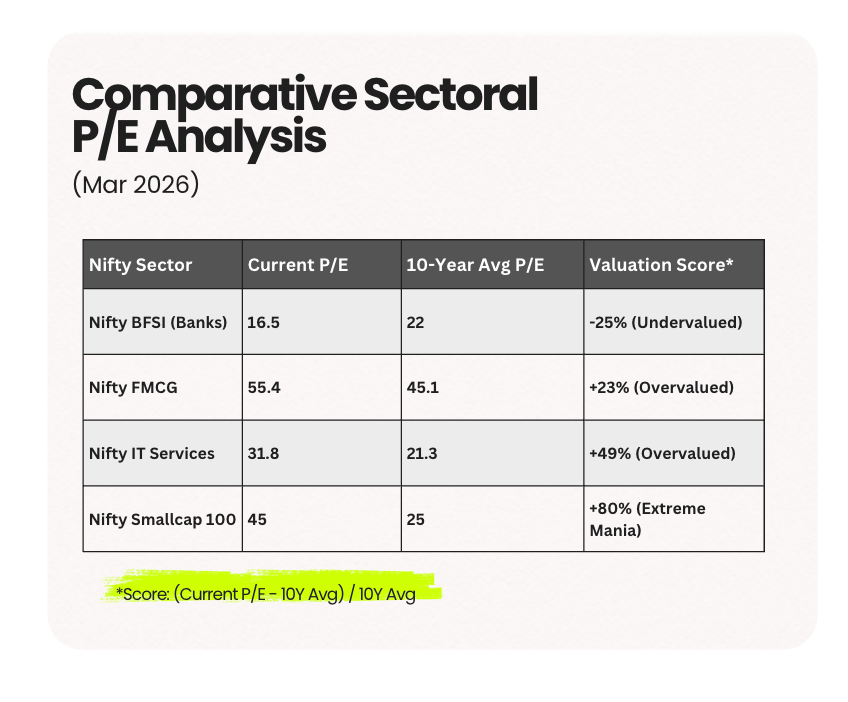

Small and Mid-Cap indices have entered "Mania" territory, trading at a 30-80% premium to their 10-year averages. Retail flows are chasing momentum, ignoring the fact that many of these companies are trading at 40x-50x P/E despite single-digit margins.

The Value Play

Conversely, Large-Cap Banking (BFSI) has cleaned up balance sheets and maintains a Credit Growth rate of 15%. Yet, it trades at a discount to its historical Price-to-Book (P/B) value, making it the most significant margin of safety play in the current market.

Section 4: 2026 Investment Playbook: Selective Discipline

We have established three key factual pillars:

- Nifty valuations (+1.8 SD) are technically overstretched.

- Core EBITDA growth (9.5%) is lagging behind P/E expansion.

- Small Caps are in Mania territory, while Banks offer structural value.

The Arbitrage Strategy: Rotation, Not Retraction

India's macro story, 7.6% real GDP growth remains the best in the world. However, being right in the country doesn't save you from being wrong on the price. The era of buying a diversified index and expecting 20% returns is over for this cycle.

Our Actionable Verdict:

- Harvest Gains: Tactically trim overweight positions in Small/Mid Caps and high-P/E IT Services where the PEG (Price/Earnings-to-Growth) ratio exceeds 2.5.

- Rotate to Value: Reallocate to Large-Cap Banking and sectors benefitting from Private Capex (Industrial Automation, Electronics).

- The Yield Gap: At a -2.74% Equity Risk Premium, it is mathematically superior to move surplus gains into Alternative Debt (11-12% yields) rather than chasing 23x P/E Large-caps.

Conclusion: India is Strategically Indispensable, not Strategically Cheap

The data confirms that India is priced for perfection. But in a world of $100 oil and shifting global rates, perfection is a fragile assumption.

- For the Nifty 50, the 26.8 P/E is NOT justified by core earnings; expect a time-correction.

- For the Small Cap Index, the 45.0 P/E is a statistical trap.

- For Large-Cap Banking, the 16.5 P/E IS justified and offers the best risk-reward profile for 2026.

India is the globally dominant growth story of the decade. It is not cheap, but it is indispensable. The key to surviving 2026 is Selective Discipline: seek the pockets where the fundamentals still match the math.